Source: The Freedonia Group, Inc.

US demand to rise about 7% annually through 2018

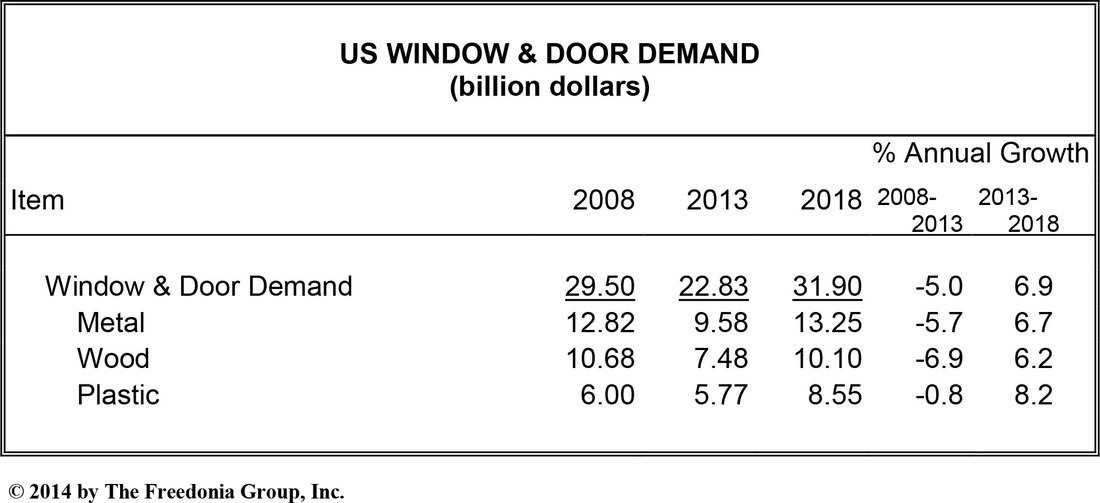

Demand for windows and doors in the US is projected to advance about seven percent per year through 2018 to $32 billion. Rebounding housing completions and building construction expenditures will stimulate gains. Construction of buildings such as residences and office, commercial, and institutional buildings that are intensive users of windows and doors is a key indicator of demand. Window and door sales saw steep declines in the 2008-2013 period due to the sharp contraction in construction spending.

Demand for windows and doors in the US is projected to advance about seven percent per year through 2018 to $32 billion. Rebounding housing completions and building construction expenditures will stimulate gains. Construction of buildings such as residences and office, commercial, and institutional buildings that are intensive users of windows and doors is a key indicator of demand. Window and door sales saw steep declines in the 2008-2013 period due to the sharp contraction in construction spending.

Plastic windows and doors to grow the fastest

Plastic windows and doors are expected to exhibit the strongest growth through 2018, increasing more than eight percent annually to $8.6 billion. Following the trend that began in the early 2000s, plastic windows and doors will continue to increase market share at the expense of wood and metal, because they offer several advantages for consumers, including low cost, minimal maintenance requirements, and superior energy performance. Plastic products, already popular in the residential market, are expected to see increasing use in light commercial and institutional applications where aesthetics, comfort, and energy efficiency are valued. Efforts by manufacturers to improve the variety of colors and woodgrain textures on plastic windows and doors or expand into markets such as specialty windows and impact resistant products will also boost plastic products, especially in nonresidential and high-end residential applications.

Metal windows and doors to remain largest segment

Metal windows accounted for over twofifths of window and door demand in 2013, the largest share of any material, and will continue to lead the market through the forecast period. However, metal products will face competition from plastic, due to the cost and energy efficiency advantages, which will limit more rapid growth. Despite increased competition, population growth in the South and West regions will support rising demand for metal products, as they are often used in those regions because heat loss through windows and doors is less of a concern. Strong growth in nonresidential construction, particularly in the institutional and office and commercial segments, where windows and doors are heavily used, will also boost demand. Metal products are installed in structures because of their durability and strength against damage or attack.

Wood windows and doors to be favored for aesthetic qualities in higher end uses

Wood window and door demand is forecast to surpass $10 billion in 2018 on 6.2 percent annual growth, the slowest of any material. Consumer perception of wood as an aesthetically pleasing material that adds value to a home will support demand, particularly in higher end residential applications. In addition, the dominance of wood in the interior door market will boost demand as building construction expenditures rise. However, like metal, wood will face strong competition from plastic window and door products. Consumer interest in plastic windows and doors over those made from wood will continue to increase because plastic products are generally more durable and require much less maintenance at a lower cost.

Study coverage

This Freedonia industry study, Windows & Doors, presents historical demand data for 2003, 2008 and 2013, plus forecasts for 2018 and 2023 by material, product, market and US region. The study also considers market environment factors, details industry structure, evaluates company market share and profiles industry players, including Andersen, Jeld-Wen, Pella, Masonite, Oldcastle, Overhead Door, ASSA ABLOY, Marivn, Fortune Brands, MI Windows and Doors and Associated Materials.

Plastic windows and doors are expected to exhibit the strongest growth through 2018, increasing more than eight percent annually to $8.6 billion. Following the trend that began in the early 2000s, plastic windows and doors will continue to increase market share at the expense of wood and metal, because they offer several advantages for consumers, including low cost, minimal maintenance requirements, and superior energy performance. Plastic products, already popular in the residential market, are expected to see increasing use in light commercial and institutional applications where aesthetics, comfort, and energy efficiency are valued. Efforts by manufacturers to improve the variety of colors and woodgrain textures on plastic windows and doors or expand into markets such as specialty windows and impact resistant products will also boost plastic products, especially in nonresidential and high-end residential applications.

Metal windows and doors to remain largest segment

Metal windows accounted for over twofifths of window and door demand in 2013, the largest share of any material, and will continue to lead the market through the forecast period. However, metal products will face competition from plastic, due to the cost and energy efficiency advantages, which will limit more rapid growth. Despite increased competition, population growth in the South and West regions will support rising demand for metal products, as they are often used in those regions because heat loss through windows and doors is less of a concern. Strong growth in nonresidential construction, particularly in the institutional and office and commercial segments, where windows and doors are heavily used, will also boost demand. Metal products are installed in structures because of their durability and strength against damage or attack.

Wood windows and doors to be favored for aesthetic qualities in higher end uses

Wood window and door demand is forecast to surpass $10 billion in 2018 on 6.2 percent annual growth, the slowest of any material. Consumer perception of wood as an aesthetically pleasing material that adds value to a home will support demand, particularly in higher end residential applications. In addition, the dominance of wood in the interior door market will boost demand as building construction expenditures rise. However, like metal, wood will face strong competition from plastic window and door products. Consumer interest in plastic windows and doors over those made from wood will continue to increase because plastic products are generally more durable and require much less maintenance at a lower cost.

Study coverage

This Freedonia industry study, Windows & Doors, presents historical demand data for 2003, 2008 and 2013, plus forecasts for 2018 and 2023 by material, product, market and US region. The study also considers market environment factors, details industry structure, evaluates company market share and profiles industry players, including Andersen, Jeld-Wen, Pella, Masonite, Oldcastle, Overhead Door, ASSA ABLOY, Marivn, Fortune Brands, MI Windows and Doors and Associated Materials.

RSS Feed

RSS Feed