Source: McGraw Hill Construction

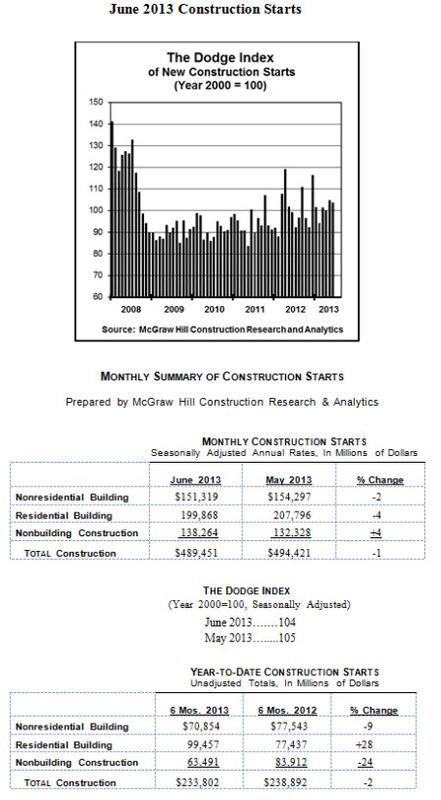

New construction starts in June receded 1% to a seasonally adjusted annual rate of $489.5 billion, according to McGraw Hill Construction, a division of McGraw Hill Financial. Nonresidential building lost momentum in June after strengthening during the previous two months, and housing experienced a pause from its recent upward trend. Meanwhile, nonbuilding construction advanced in June, lifted by the start of several very large bridge projects. For the first six months of 2013, total construction starts on an unadjusted basis were reported at $233.8 billion, down 2% from the same period a year ago. The 2013 year-to-date decline for total construction was due primarily to a sharp reduction for electric utilities compared to a robust first half of 2012. If electric utilities are excluded, total construction starts for the first six months of 2013 would be up 9% from last year, led by substantial growth for housing.

June’s construction start statistics produced a reading of 104 for the Dodge Index (2000=100), compared to 105 for May. During the first four months of 2013, the Dodge Index averaged 99, slightly below its full year average for 2012 at 101, so May and June provided some evidence that the pace of construction starts is beginning to pick up. “The first half of 2013 revealed a mixed performance by project type, producing a hesitant pattern for total construction starts,” stated Robert A. Murray, vice president of economic affairs for McGraw Hill Construction. “On the plus side, the housing market continues to strengthen, and it should be able to register further gains this year even with the recent hike in mortgage rates. Commercial building continues to slowly advance, and public works construction to this point has not seen much dampening as the result of the sequester. However, on the negative side, the retreat for institutional building has turned out to be steeper than expected, manufacturing plant construction has weakened, and new electric utility starts have plunged from last year’s record pace. Assuming the downward pull from the negative sectors in this year’s first half becomes less severe in the second half, then total construction starts for all of 2013 should still be able to register growth, but at just a single-digit pace in similarity to 2012.”

Nonresidential building in June slipped 2% to $151.3 billion (annual rate), retreating slightly after May’s 9% gain. The institutional sector in June showed diminished activity for healthcare facilities, down 13%, as hospital mergers and the uncertainty related to the implementation of the Affordable Care Act continue to restrain construction. The largest healthcare projects reported as June starts were valued at $200 million or less, including a $200 million critical care tower in Akron OH and a $114 million renovation to a university medical center in New York NY. The public buildings category in June plummeted 33% from its briefly improved volume in May, returning to the weak amount witnessed earlier this year. The educational buildings category in June managed to strengthen 11%, suggesting that it’s now leveling off after particularly weak activity in recent months. Large educational building projects that reached groundbreaking in June included a $252 million academic building for the New York City College of Technology in Brooklyn NY, an $81 million middle school in Pennsylvania, and an $80 million high school addition in Connecticut. Amusement-related construction increased 2% in June, while larger gains were reported for two of the smaller institutional categories from depressed activity in May – transportation terminals, up 24%; and churches, up 29%.

The commercial sector in June showed varied behavior. Office construction jumped 44%, led by the June start of an $861 million computing center for the U.S. Army at Fort Meade MD. Other large office projects that were reported as June starts were the $200 million Samsung American Headquarters in San Jose CA and a $110 million office complex in Richmond VA. Hotel construction in June dropped 29% after an elevated May amount, with June’s decline cushioned by the start of a $185 million hotel/casino renovation in Las Vegas NV. Both stores and warehouses slipped back in June, falling 6% and 7% respectively. The manufacturing plant category in June fell 19% after a strong May, with the largest June projects being a $175 million iron ore pellet plant in Indiana and a $165 million refinery expansion in Salt Lake City UT.

During the first six months of 2013, nonresidential building decreased 9% from a year ago. The institutional sector dropped 13%, including these year-to-date declines – educational buildings, down 12%; healthcare facilities, down 18%; and public buildings, down 34%. The manufacturing plant category in this year’s January-June period fell 29%, reflecting the comparison to a first half of 2012 that included such projects as a $375 million petrochemical plant in Louisiana and a $346 million metals processing plant in North Carolina. In contrast, the commercial categories in this year’s first half climbed 3%, with hotels up 28%, warehouses up 6%, and office buildings up 1%, although stores dropped 7%. The year-to-date decline for stores was relative to a first half of 2012 that included the $400 million renovation of Macy’s flagship store in New York NY. Murray noted, “As 2013 progresses, it’s expected that the gap for nonresidential building relative to last year will narrow, since the comparison will include the slower pace for nonresidential building that occurred during the latter half of 2012.”

Residential building, at $199.9 billion (annual rate), dropped 4% in June. Multifamily housing fell 20%, after moving at a particularly fast clip during the first five months of this year. The June level for multifamily housing was still relatively healthy by recent standards – just 2% below its average monthly pace during 2012. Large multifamily projects that reached groundbreaking in June included a $140 million residential tower in Boston MA, a $125 million residential tower in Jersey City NJ, the $91 million apartment portion of the Chinese Foreign Mission and Residential Building in Washington DC, and an $85 million apartment complex in Fredericksburg VA. Single family housing in June edged up 1%, maintaining the strengthening trend that’s been present since mid-2011. The June amount for single family housing was up 29% from its average monthly pace during 2012.

At the six-month mark of 2013, residential building in dollar terms advanced 28% from the first half of 2012, with single family housing climbing 31% while multifamily housing grew 19%. For single family housing, the year-to-date gains were widespread by geography, with all five major regions of the U.S. reporting double-digit increases compared to a year ago – the South Atlantic, up 42%; the West, up 33%; the Midwest, up 31%; the Northeast, up 24%; and the South Central, up 21%. For multifamily housing, the top five metropolitan markets during the first half of 2013 ranked by the dollar amount of new projects (with the percent change from a year ago) were – New York NY, up 51%; Washington DC, down 4%; Miami FL, up 59%; Boston MA, up 46%; and Los Angeles CA, down 52%. Multifamily metropolitan markets ranked 6 through 10 during the first half of 2013 were – Denver CO, up 55%; Atlanta GA, up 127%; Chicago IL, up 77%; Phoenix AZ, up 98%; and Dallas-Ft. Worth TX, down 20%.

Nonbuilding construction in June increased 4% to $138.3 billion (annual rate). The public works portion of nonbuilding construction jumped 38%, led by a 164% surge for bridge construction. The largest project that lifted the bridge total for June was $1.6 billion for work on the Ohio River Bridges in the Louisville KY and southern Indiana area. Other large bridge projects that were reported as June construction starts were the $255 million restoration of the Longfellow Bridge in Boston MA, a $209 million bridge as part of the Grand Parkway expansion in the Houston TX area, and the $93 million deck replacement for the Newburgh-Beacon Bridge in Beacon NY. Highway construction in June advanced 25% from the previous month, boosted by $832 million for work on the Houston area’s Grand Parkway project. The miscellaneous public works category, which includes such diverse project types as pipelines and site work, climbed 60% in June. Large projects aiding the miscellaneous public works total included a $350 million natural gas pipeline in Maine and $150 million for pilings at the site of the upcoming Tappan Zee Bridge replacement project in the Tarrytown NY area. On the environmental side, sewer-related construction increased 63% from a weak May, helped by the start of a $163 million biosolids handling plant in Irvine CA. River/harbor development in June retreated 9%, despite $122 million for phase 3 of the Miami FL harbor deepening project, while water supply construction dropped 37%. Electric utility construction in June fell 78%, running counter to the general strength shown by public works.

For the first six months of 2013, nonbuilding construction dropped 24% compared to last year. The electric utility category plunged 70%, reflecting the comparison to the first half of 2012 that included $8.5 billion for Units 3 and 4 at the Vogtle nuclear power facility in Georgia, $8.5 billion for Units 2 and 3 at the V.C. Summer nuclear power facility in South Carolina, plus several very large gas-fired, solar, and wind power facilities. Public works construction in the first six months of 2013 increased 6%. Highways and bridges strengthened relative to a sluggish first half of 2012, rising 10% and 27% respectively. Year-to-date gains were also reported for river/harbor development, up 20%; and water supply systems, up 14%. Declines relative to the first half of last year were reported for sewers, down 11%; and miscellaneous public works, down 12%.

The 2% downturn for total construction starts at the U.S. level during the first six months of 2013 came from a varied pattern by geography. Greater activity for total construction was reported for the South Central, up 8%; the Northeast, up 7%; and the West, up 4%. Decreased activity for total construction was reported for the Midwest, down 5%; and the South Atlantic, down 18%. If electric utilities are excluded from the construction start statistics in the South Atlantic, that region would register a 21% year-to-date gain.

Nonresidential building in June slipped 2% to $151.3 billion (annual rate), retreating slightly after May’s 9% gain. The institutional sector in June showed diminished activity for healthcare facilities, down 13%, as hospital mergers and the uncertainty related to the implementation of the Affordable Care Act continue to restrain construction. The largest healthcare projects reported as June starts were valued at $200 million or less, including a $200 million critical care tower in Akron OH and a $114 million renovation to a university medical center in New York NY. The public buildings category in June plummeted 33% from its briefly improved volume in May, returning to the weak amount witnessed earlier this year. The educational buildings category in June managed to strengthen 11%, suggesting that it’s now leveling off after particularly weak activity in recent months. Large educational building projects that reached groundbreaking in June included a $252 million academic building for the New York City College of Technology in Brooklyn NY, an $81 million middle school in Pennsylvania, and an $80 million high school addition in Connecticut. Amusement-related construction increased 2% in June, while larger gains were reported for two of the smaller institutional categories from depressed activity in May – transportation terminals, up 24%; and churches, up 29%.

The commercial sector in June showed varied behavior. Office construction jumped 44%, led by the June start of an $861 million computing center for the U.S. Army at Fort Meade MD. Other large office projects that were reported as June starts were the $200 million Samsung American Headquarters in San Jose CA and a $110 million office complex in Richmond VA. Hotel construction in June dropped 29% after an elevated May amount, with June’s decline cushioned by the start of a $185 million hotel/casino renovation in Las Vegas NV. Both stores and warehouses slipped back in June, falling 6% and 7% respectively. The manufacturing plant category in June fell 19% after a strong May, with the largest June projects being a $175 million iron ore pellet plant in Indiana and a $165 million refinery expansion in Salt Lake City UT.

During the first six months of 2013, nonresidential building decreased 9% from a year ago. The institutional sector dropped 13%, including these year-to-date declines – educational buildings, down 12%; healthcare facilities, down 18%; and public buildings, down 34%. The manufacturing plant category in this year’s January-June period fell 29%, reflecting the comparison to a first half of 2012 that included such projects as a $375 million petrochemical plant in Louisiana and a $346 million metals processing plant in North Carolina. In contrast, the commercial categories in this year’s first half climbed 3%, with hotels up 28%, warehouses up 6%, and office buildings up 1%, although stores dropped 7%. The year-to-date decline for stores was relative to a first half of 2012 that included the $400 million renovation of Macy’s flagship store in New York NY. Murray noted, “As 2013 progresses, it’s expected that the gap for nonresidential building relative to last year will narrow, since the comparison will include the slower pace for nonresidential building that occurred during the latter half of 2012.”

Residential building, at $199.9 billion (annual rate), dropped 4% in June. Multifamily housing fell 20%, after moving at a particularly fast clip during the first five months of this year. The June level for multifamily housing was still relatively healthy by recent standards – just 2% below its average monthly pace during 2012. Large multifamily projects that reached groundbreaking in June included a $140 million residential tower in Boston MA, a $125 million residential tower in Jersey City NJ, the $91 million apartment portion of the Chinese Foreign Mission and Residential Building in Washington DC, and an $85 million apartment complex in Fredericksburg VA. Single family housing in June edged up 1%, maintaining the strengthening trend that’s been present since mid-2011. The June amount for single family housing was up 29% from its average monthly pace during 2012.

At the six-month mark of 2013, residential building in dollar terms advanced 28% from the first half of 2012, with single family housing climbing 31% while multifamily housing grew 19%. For single family housing, the year-to-date gains were widespread by geography, with all five major regions of the U.S. reporting double-digit increases compared to a year ago – the South Atlantic, up 42%; the West, up 33%; the Midwest, up 31%; the Northeast, up 24%; and the South Central, up 21%. For multifamily housing, the top five metropolitan markets during the first half of 2013 ranked by the dollar amount of new projects (with the percent change from a year ago) were – New York NY, up 51%; Washington DC, down 4%; Miami FL, up 59%; Boston MA, up 46%; and Los Angeles CA, down 52%. Multifamily metropolitan markets ranked 6 through 10 during the first half of 2013 were – Denver CO, up 55%; Atlanta GA, up 127%; Chicago IL, up 77%; Phoenix AZ, up 98%; and Dallas-Ft. Worth TX, down 20%.

Nonbuilding construction in June increased 4% to $138.3 billion (annual rate). The public works portion of nonbuilding construction jumped 38%, led by a 164% surge for bridge construction. The largest project that lifted the bridge total for June was $1.6 billion for work on the Ohio River Bridges in the Louisville KY and southern Indiana area. Other large bridge projects that were reported as June construction starts were the $255 million restoration of the Longfellow Bridge in Boston MA, a $209 million bridge as part of the Grand Parkway expansion in the Houston TX area, and the $93 million deck replacement for the Newburgh-Beacon Bridge in Beacon NY. Highway construction in June advanced 25% from the previous month, boosted by $832 million for work on the Houston area’s Grand Parkway project. The miscellaneous public works category, which includes such diverse project types as pipelines and site work, climbed 60% in June. Large projects aiding the miscellaneous public works total included a $350 million natural gas pipeline in Maine and $150 million for pilings at the site of the upcoming Tappan Zee Bridge replacement project in the Tarrytown NY area. On the environmental side, sewer-related construction increased 63% from a weak May, helped by the start of a $163 million biosolids handling plant in Irvine CA. River/harbor development in June retreated 9%, despite $122 million for phase 3 of the Miami FL harbor deepening project, while water supply construction dropped 37%. Electric utility construction in June fell 78%, running counter to the general strength shown by public works.

For the first six months of 2013, nonbuilding construction dropped 24% compared to last year. The electric utility category plunged 70%, reflecting the comparison to the first half of 2012 that included $8.5 billion for Units 3 and 4 at the Vogtle nuclear power facility in Georgia, $8.5 billion for Units 2 and 3 at the V.C. Summer nuclear power facility in South Carolina, plus several very large gas-fired, solar, and wind power facilities. Public works construction in the first six months of 2013 increased 6%. Highways and bridges strengthened relative to a sluggish first half of 2012, rising 10% and 27% respectively. Year-to-date gains were also reported for river/harbor development, up 20%; and water supply systems, up 14%. Declines relative to the first half of last year were reported for sewers, down 11%; and miscellaneous public works, down 12%.

The 2% downturn for total construction starts at the U.S. level during the first six months of 2013 came from a varied pattern by geography. Greater activity for total construction was reported for the South Central, up 8%; the Northeast, up 7%; and the West, up 4%. Decreased activity for total construction was reported for the Midwest, down 5%; and the South Atlantic, down 18%. If electric utilities are excluded from the construction start statistics in the South Atlantic, that region would register a 21% year-to-date gain.

RSS Feed

RSS Feed