Source: The American Institute of Architects By Jennifer Riskus

More than half of firms report increased productivity in recent years

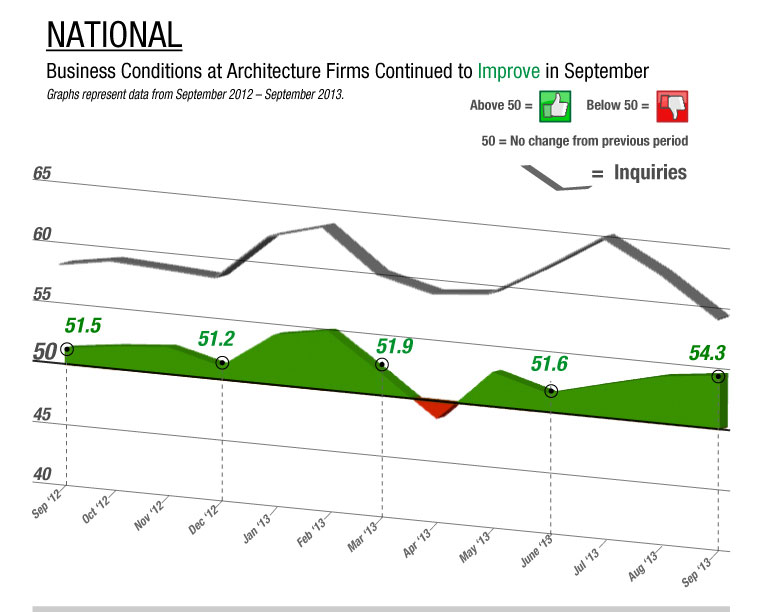

Business conditions continued to improve at architecture firms in September, with the AIA’s Architecture Billings Index (ABI) score rising to 54.3. (Any score above 50 indicates billings growth). Despite uncertainty in the general economy related to the federal government shutdown, firm billings have been accelerating every month since the beginning of the summer. Inquiries into new work continue to rise, despite having dipped slightly from their most recent high earlier this year, and the value of new design contracts increased in September as well.

Smaller employment gains, but bright spots in construction, architectural services

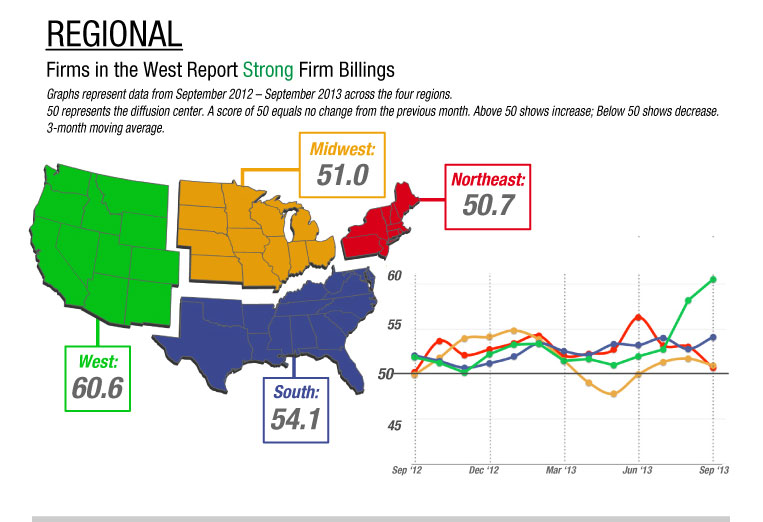

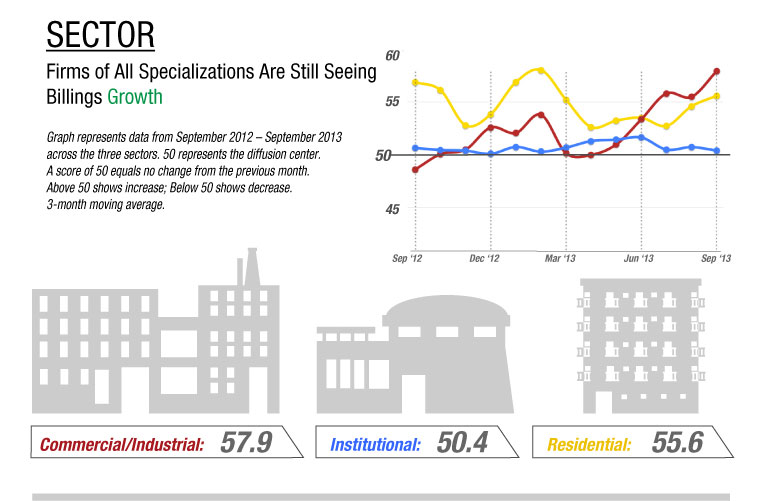

Business conditions remained strong at firms in all regions of the country in September, with firms located in the South and West regions showing the strongest growth for the second month in a row. Firm billings remained particularly strong at firms located in the West, as they continue to rebound from the recession that plagued them longer than most other regions of the country. Billings also continued to rise at firms of all specializations. Growth has softened slightly from earlier in the year at firms with a residential specialization, but business conditions continued to improve for firms with a commercial/industrial specialization. Firms that focus on institutional sector work are still reporting only modest improvements in billings.

With the partial federal government shutdown in early October, the release of much of the data that the construction industry uses to gauge the state of the economy was delayed, so economists are only now starting to get a sense of what transpired in the broader economy in September. The most recent edition of the Federal Reserve’s Beige Book of regional economic trends was released on Oct. 16, and covers the period of September through the first week of October. The report shows a generally positive outlook across much of the country, with both residential and nonresidential construction expanding in most areas, but notes that the partial government shutdown and debate over increasing the debt ceiling have increased uncertainty in many areas. Residential construction grew at a stronger pace than nonresidential construction overall, but nonresidential construction showed strong growth in the Minneapolis District, and more modest growth in the Richmond, Atlanta, and Philadelphia Districts. The commercial real estate outlook remains mostly positive, supported by falling vacancy rates and rising rents.

Employment gains were smaller in September, with only 148,000 new jobs added, down nearly 40,000 from average monthly gains over the previous 12 months. However, construction payrolls added 20,000 new jobs for the month, while architectural services increased by 1,300 to 156,000 in August (the most recent data available). This is the highest architectural services payrolls have been since the spring.

Productivity during recession

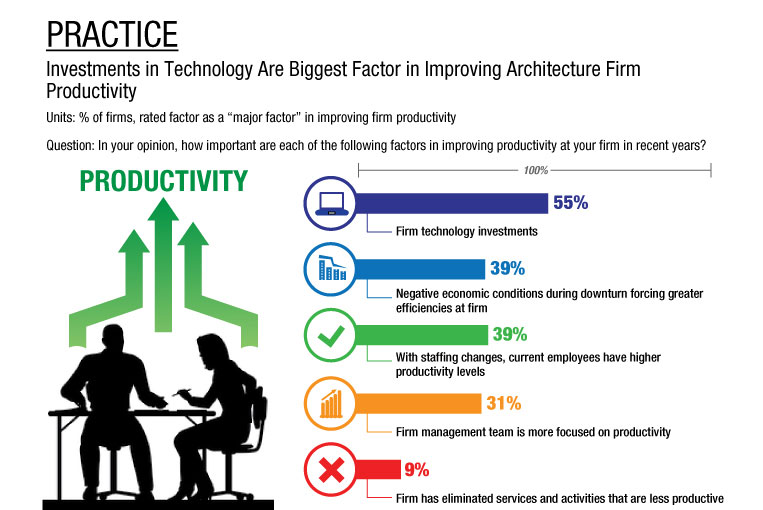

As architecture firms recover from the Great Recession, many have found that their firm-wide productivity levels (measured as output per hour of labor) have increased. In response to this month’s special practice question, more than half of firms (53 percent) reported that their productivity levels increased over the past few years, compared to 22 percent who estimated that their productivity levels decreased. The remaining 25 percent have seen productivity levels remain about the same. A higher share of large firms report increased productivity levels, with 60 percent of firms with annual billings over $5 million reporting an increase in productivity. This is compared to only 50 percent of firms with annual billings of less than $250,000 who report increasing productivity.

Firms that indicated they experienced increased productivity were asked to rate the importance of various factors in improving their output. More than half of firms (55 percent) reported that firm technology investments (such as BIM, communications equipment, and other software/hardware) were a major factor in increasing their productivity. Thirty-nine percent of firms found that negative economic conditions during the downturn, which forced greater efficiencies at the firm, were a major factor, and 39 percent of firms also rated higher productivity levels due to staffing changes as a major factor. Additionally, firms indicated that eliminating less productive services/activities was generally not a factor in increasing productivity.

This month, Work-On-The-Boards participants are saying:

Smaller employment gains, but bright spots in construction, architectural services

Business conditions remained strong at firms in all regions of the country in September, with firms located in the South and West regions showing the strongest growth for the second month in a row. Firm billings remained particularly strong at firms located in the West, as they continue to rebound from the recession that plagued them longer than most other regions of the country. Billings also continued to rise at firms of all specializations. Growth has softened slightly from earlier in the year at firms with a residential specialization, but business conditions continued to improve for firms with a commercial/industrial specialization. Firms that focus on institutional sector work are still reporting only modest improvements in billings.

With the partial federal government shutdown in early October, the release of much of the data that the construction industry uses to gauge the state of the economy was delayed, so economists are only now starting to get a sense of what transpired in the broader economy in September. The most recent edition of the Federal Reserve’s Beige Book of regional economic trends was released on Oct. 16, and covers the period of September through the first week of October. The report shows a generally positive outlook across much of the country, with both residential and nonresidential construction expanding in most areas, but notes that the partial government shutdown and debate over increasing the debt ceiling have increased uncertainty in many areas. Residential construction grew at a stronger pace than nonresidential construction overall, but nonresidential construction showed strong growth in the Minneapolis District, and more modest growth in the Richmond, Atlanta, and Philadelphia Districts. The commercial real estate outlook remains mostly positive, supported by falling vacancy rates and rising rents.

Employment gains were smaller in September, with only 148,000 new jobs added, down nearly 40,000 from average monthly gains over the previous 12 months. However, construction payrolls added 20,000 new jobs for the month, while architectural services increased by 1,300 to 156,000 in August (the most recent data available). This is the highest architectural services payrolls have been since the spring.

Productivity during recession

As architecture firms recover from the Great Recession, many have found that their firm-wide productivity levels (measured as output per hour of labor) have increased. In response to this month’s special practice question, more than half of firms (53 percent) reported that their productivity levels increased over the past few years, compared to 22 percent who estimated that their productivity levels decreased. The remaining 25 percent have seen productivity levels remain about the same. A higher share of large firms report increased productivity levels, with 60 percent of firms with annual billings over $5 million reporting an increase in productivity. This is compared to only 50 percent of firms with annual billings of less than $250,000 who report increasing productivity.

Firms that indicated they experienced increased productivity were asked to rate the importance of various factors in improving their output. More than half of firms (55 percent) reported that firm technology investments (such as BIM, communications equipment, and other software/hardware) were a major factor in increasing their productivity. Thirty-nine percent of firms found that negative economic conditions during the downturn, which forced greater efficiencies at the firm, were a major factor, and 39 percent of firms also rated higher productivity levels due to staffing changes as a major factor. Additionally, firms indicated that eliminating less productive services/activities was generally not a factor in increasing productivity.

This month, Work-On-The-Boards participants are saying:

• New project levels have been [quickly] increasing for most of 2013. We hope the government shutdown does not affect clients’ long term projections.

—25-person firm in the South, commercial/industrial specialization

• Projects, other than state-funded [ones], are beginning to flow again. However, owners are more cost-conscious, and often shortlist less-qualified firms with much lower fees with whom we must compete.

—15-person firm in the Northeast, institutional specialization

• We have observed an upturn in inquiries in all areas of our practice, with private and government projects proposed as we go into the last quarter of this year and the first half of next.

—10-person firm in the Midwest, commercial/industrial specialization

• We have increased staff 40 percent, and have the largest backlog in firm history. The immediate future seems solid.

— 120-person firm in the West, institutional specialization

—25-person firm in the South, commercial/industrial specialization

• Projects, other than state-funded [ones], are beginning to flow again. However, owners are more cost-conscious, and often shortlist less-qualified firms with much lower fees with whom we must compete.

—15-person firm in the Northeast, institutional specialization

• We have observed an upturn in inquiries in all areas of our practice, with private and government projects proposed as we go into the last quarter of this year and the first half of next.

—10-person firm in the Midwest, commercial/industrial specialization

• We have increased staff 40 percent, and have the largest backlog in firm history. The immediate future seems solid.

— 120-person firm in the West, institutional specialization

RSS Feed

RSS Feed